As competitive markets evolve, companies must avoid ending up in the “ditch.” Based on the forthcoming book, The Rule of Three: Surviving & Thriving in Competitive Markets (New York: Free Press, 2002)

Abstract

Competitive markets evolve in a predictable manner and, once mature, exhibit many similarities across industries and geographies. Most notably, each market tends to be dominated by three major, volume-driven firms, which we term “full-line generalists,” surrounded by a constellation of smaller margin-driven firms that are either product or market specialists. The three large firms together control approximately 70% to 90% of the market; niche players serve the balance. Further, a company needs a market share of at least 10% to be viable as a full-line generalist. In between the generalists and specialists is a gap, representing a market share of between 5% and 10%. It is in this “ditch” that efficiency suffers and financial performance tends to be weakest relative to other levels of market share. The strategic implications of the “Rule of Three” are myriad. Marginal full-line players (those with market shares close to 10%) are in danger of being pushed into the ditch by the larger players. Specialists that grow unwisely are in danger of being pulled into the ditch by the lure of greater market share. Particular competitive strategies spell success at various levels within a market; we present distinct strategies that companies need to pursue, depending on whether they are No. 1, No. 2, No. 3, ditch-dwelling or specialist players.

Introduction

Over the past several years, the world economy, principally in the developed free market economies of North America and Europe, has witnessed a unique combination of economic phenomena: mergers as well as demergers (i.e., spin-offs of non-core businesses) at record levels. Every year between 1997 and 2000 saw new records established for mergers as well as demergers. As a result, the landscape of just about every major industry has changed in a significant way. Industries as varied as wireless communications (Vodaphone merging with Mannesman), aluminum, banking, pharmaceuticals (the merger between Glaxo Wellcome and SmithKline Beecham to form the world’s No. 1 drug company), petroleum (the merger of Exxon and Mobil) and airlines are in the midst of rationalization and consolidation, moving inexorably toward what we call the Rule of Three. The recent economic downturn has slowed but not halted this fundamental evolution, nor has it altered its basic direction.

What is the Rule of Three?

Just as living organisms have a reasonably standard pattern of growth and development, so do competitive markets, and our research into approximately 200 industries has revealed that markets evolve in a highly predictable fashion, governed by the “Rule of Three.”

Through competitive market forces, markets that are largely free of regulatory constraints and major entry barriers (such as very restrictive patent rights or government-controlled capacity licenses) eventually get organized into two kinds of competitors: full-line generalists and product/market specialists. Full line generalists compete across a range of products and markets, and are volume-driven players for whom financial performance improves with gains in market share. Specialists tend to be margin-driven players, which actually suffer deterioration in financial performance by increasing their share of the broad market. Contrary to traditional economic theory, then, evolved markets tend to be simultaneously oligopolistic as well as monopolistic.

Figure 1: The Rule Of Three

The accompanying figure plots financial performance and market share, illustrating the central paradigm of the Rule of Three: in competitive, mature markets, there is only room for three full-line generalists, along with several (in some markets, numerous) product or market specialists. Together, the three “inner circle” competitors typically control, in varying proportions, between 70% and 90% of the market. To be viable as volume-driven players, companies must have a critical-mass market share of at least 10%. As the illustration shows, the financial performance of full- line generalists gradually improves with greater market share, while the performance of specialists drops off rapidly as their market share increases.

There is a discontinuity “in the middle;” mid-sized companies almost always exhibit the worst financial performance of all. We label this middle position the “ditch,” the competitive pothole in the market (generally between 5% and 10% market share) where competitive position (and, thus, financial performance) is the weakest. The rule of competitive market physics is very simple–those closest to the ditch are the ones most likely to fall into it. Therefore, the most desirable competitive positions are those furthest away from the middle. Firms on either side of the ditch–especially those close to it–need to develop strategies to distance themselves. If a firm in a mature industry finds itself in the ditch, it must carefully consider its options and formulate an explicit strategy to move either to the right or the left.

The Rule of Three applies (and renews itself) at every stage of a market’s geographic evolution–from local to regional, regional to national, and national to global.

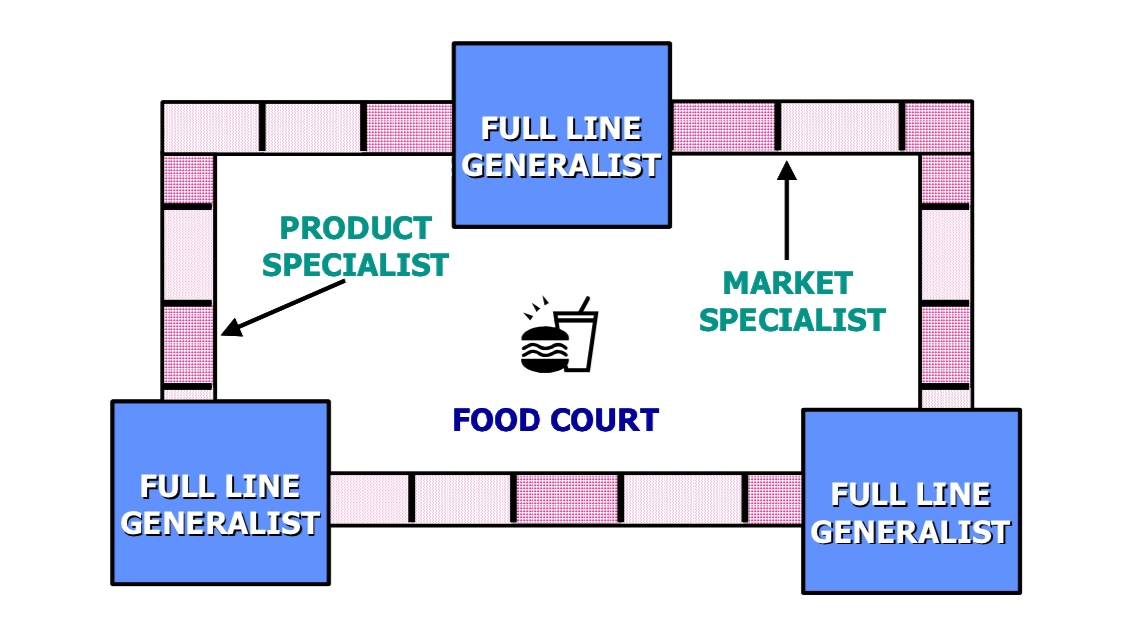

Figure 2: The Shopping Mall Analogy

A useful analogy to mature competitive markets is a shopping mall (Figure 2).

Mature markets are “anchored” by a few full-line generalists, which are akin to the full-service anchor department stores (such as Sears and JC Penney) in a mall.

In addition, a number of other players are positioned as either product specialists or market specialists. In a mall, a store such as Footlocker is clearly a product specialist, while The Limited is more of a market specialist. While Footlocker sells only athletic shoes, The Limited has a precisely-defined target market–young, affluent, educated, professional women–and caters to a wide range of their fashion needs. Store image, customer image and employee image all blend into one homogenous mix. The same company likewise operates stores such as Victoria’s Secret, Lane Bryant and Limited Express, each a market specialist targeting a different customer group. This structure illustrates a maxim that we will discuss later–that the best way for a specialist to grow profitably is through the spawning of new specialists.

How Competitive Markets Evolve

By observing how numerous markets have evolved, we have identified the primary drivers of change and a pattern of evolution. In the auto industry’s late 19th century infancy, for example, some 500 manufacturers were building cars in the U.S. alone, none on a truly national scale. It took the 1909 launch of the Model T and Henry Ford’s innovations in mass production to establish a standard and initiate the process of industry consolidation. By 1917, the number of manufacturers dwindled to just 23; by the 1940s, the market had consolidated further into three full-line players (GM, Ford and Chrysler) and several niche players such as American Motors

(which failed in its attempts at becoming a generalist and was acquired by Renault and then by Chrysler), Checker and Studebaker.

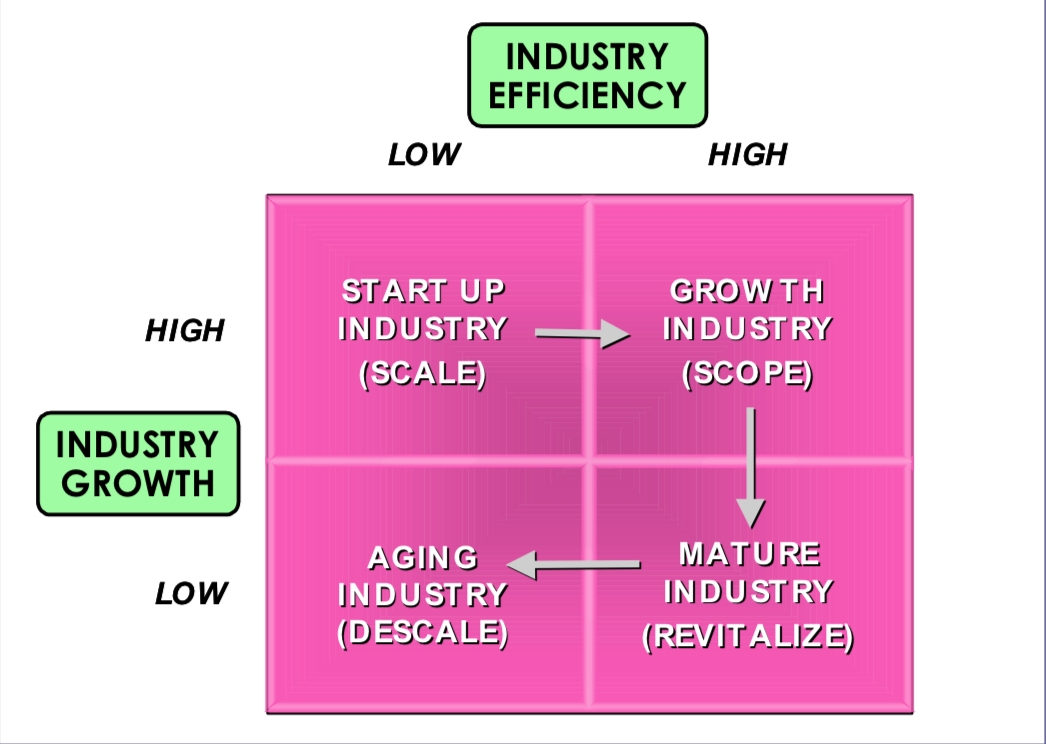

Figure 3: How Markets Evolve

Eventually, the Rule of Three prevailed, with GM, Ford and Chrysler dominating the U.S. market.

Two driving forces shape markets: efficiency and growth (Figure 3). Growth comes primarily from creating customer demand while efficiency is a function of optimized operations. In cyclical pursuit of these objectives, markets get organized and reorganized over time.

The starting point for a new market is almost always a new technology. Although early entrants can specialize in different ways, almost all tend to be product specialists. Young markets tend to have few technical standards, low barriers to entry and exit, and a decidedly local geographic focus. Newly created markets are typified by rapid growth and the presence of numerous competitors jockeying for position. This quickly leads to excess capacity as the market attracts more entrants than it can support.

Even though viable start-up markets grow rapidly in pursuit of scale economies, they tend to be highly inefficient; firms within the industry lack economies of scale, operational experience and tools to automate production and distribution tasks. They tend to be vertically integrated, producing many of their own inputs, since a well-defined supply function has yet to emerge in the fledgling industry. Consequently, during the growth phase, the drivers of market evolution are geared to creating efficiency by enhancing scale economies and lowering costs. There are four key processes by which this happens:

- Creation of Standards: Market processes often result in the creation of a de facto standard. The standard could be for products (as with MS-DOS in personal computing) or processes (as with the assembly-line manufacturing process pioneered for the Model T).

- Shared Infrastructure: The market might also create efficiency through the development of a shared infrastructure. Infrastructure costs are generally too high to be loaded on to the transactions generated by any one company. Consequently, the government may take the lead in creating or organizing the infrastructure, or one company could develop an infrastructure for its internal needs and then make it widely available. For example, banks benefit greatly from shared infrastructures for check clearing, credit card transactions and automated teller networks. Airlines require shared infrastructures for reservations, air traffic control and ground services.

- Governmental Intervention: If it sees that an important market is failing to achieve efficiency on its own, the government may intervene. In the U.S., this occurred in the telephone and railroad markets when too many companies started laying cable and setting up tracks. Each one wanted monopoly power and so made itself incompatible with the others. The government intervened and created standards and sanctioned “natural monopolies” to generate efficiency.

- Consolidation: Finally, market processes create efficiency in a highly fragmented market through the consolidation of small, inefficient players into larger ones.

Eventually, market growth begins to slow down and the drive for efficiency transforms an unorganized market with many players into an organized one with far fewer players. After a start up industry achieves a high level of efficiency through the realization of scale economies, the focus shifts toward the achievement of scope economies. This typically occurs through market expansion (from local to global) and/or product line expansion (from specialty to full line).

When a market is in its infancy, all the players are on the left side of Figure 1. Then, one player makes the turn and becomes a broad-based supplier, through acquisitions (as General Motors did in the automobile industry), the creation of a de facto standard, etc. It is at this point in the market’s natural evolution toward the Rule of Three manifests itself, allowing room for two additional players to evolve into full-line generalists.

Over time, as growth slows and the industry becomes mature, the forces of technological change, shifting regulations, market shifts and changing investor expectations may give rise to a “revolution” or revitalization of the industry. Through such periodic upheavals, the potential exists for the competitive landscape to be redrawn in a substantially different way. Savvy incumbents are able to sustain or improve on their leadership positions, while aggressive newcomers replace others.

Some industries eventually enter a phase wherein growth slows dramatically and industry efficiency declines. Survivors in such industry focus on improving financial performance through “descaling” processes such as capacity reduction, the outsourcing of non-core functions, the breakup of vertical integration and/or exiting the industry and focusing resources elsewhere.

Common Elements in Market Evolution

By analyzing the evolution of about 200 competitive markets, we have arrived at the following generalizations:

- A typical competitive market starts out in an unorganized way, with only small players serving it. As markets expand, they get organized through a process of consolidation and standardization. This process eventually results in the emergence of a small handful of “full-line generalists” surrounded by a number of “product specialists“ and “market specialists.” Contrary to the prevailing wisdom that they only occur when an industry matures or shrinks, such shakeouts often take place during market expansion (witness the cellular telephony industry in recent years).

- With uncanny regularity, the number of full-line generalists that survive this transition is three. In the typical market, the market shares of the three eventually hover around 40%, 20% and 10%, respectively. Together, they generally serve between 70% and 90% of the market, with the balance going to product/market specialists. We have found that the extent of market share concentration among the big three depends on the extent to which fixed costs dominate the cost structure.

- TheRule of Three applies (and renews itself) at every stage of a market’s geographic evolutionfrom local to regional, regional to national, and national to global.

- The financial performance of the three large players improves with increased marketshare–up to a point (typically 40%). Beyond that point, diseconomies of scale set in, along with the potential for regulatory problems related to heightened anti-monopoly scrutiny.

- The big three companies are typically valued at a premium (measured by the price-earnings ratio) compared with smaller companies, especially those in the ditch. The oil industry is a recent example; the global “Big Three” (Exxon-Mobil, BP and Royal Dutch) have P/E ratios of 15, 18 and 13 respectively, while mid-sized players Texaco, Chevron, Philips and Conoco have P/E ratios of 12, 9, 6 and 7 respectively.

- If the top player commands 70% or more of the market (usually because of a proprietary technology or strong patent rights), there is often no room for even a second full-line generalist. When IBM dominated the mainframe business many years ago, all of its competitors had to become niche players to survive. When the market leader has a share between 50 and 70%, there is often only room for two full- line generalists. Similarly, if the market leader enjoys considerably less than 40%, there may (temporarily) be room for a fourth generalist player.

- A market share of 10% is the minimum level necessary for a player to be viable as a full-line generalist. Companies that dip below this level are not viable as full-line players, and must make the transition to specialist status to survive; alternatively, they must consider a merger with another company to regain a market share above 10%. In the US airline industry, US Airways, Northwest and America West are all in the ditch; each will eventually have to shrink into specialty status or merge with one of the Big Three (American, United and Delta) in order to survive. Previous ditch players, such as Eastern, Braniff, PanAm and TWA, have already perished.

- In a market suffering through a downturn in growth, the fight for market share between Nos. 1 and 2 often sends the No. 3 company into the ditch. For example, this happened in soft drinks (RC Cola wound up in the ditch), beer (Schlitz), aircraft manufacturing (Lockheed first, then McDonnell Douglas), and automobiles (previous battles between GM and Ford drove Chrysler perilously close to extinction).

- Nevertheless,inthelongrun,anewNo.3full-lineplayeralwaysemerges.Intheglobalizedsoftdrink market currently, the combination of Cadbury-Schweppes, Dr. Pepper and 7-Up has resulted in the creation of a viable new No. 3 player behind Coke and Pepsi, with approximately 17% market share.

- The number one company is usually the least innovative, though it may have the largest R&D budget. Such companies tend to adopt a “fast follower” strategic posture when it comes to innovation.

- The number three company is usually the most innovative. However, its innovations are usually “stolen” by the number one company unless it can protect them. Such protection becomes more difficult to attain over time.

- The extent to which the third ranked player enjoys a comfortable or precarious existence depends on how far away that player is from the “ditch.”

- The performance of specialist companies deteriorates as they grow market share within the overall market, but improves as they grow their share of a specialty niche.

- Reckless growth can rapidly lead specialists into the ditch. The airline PeopleExpress is a classic example; after a few years of heady growth, the Newark (NJ)-based carrier flamed out as it sought to add flights across the continent and to Europe.

- Specialists can make the transition to successful full line generalists only if there are two or fewer incumbent generalists in the market.

- Alternatively, specialists serving a niche that has gone mainstream can sell out to full line generalists, as Mennon, Maybeline and Gatorade have done.

- Successful product or market specialists typically face only one direct competitor in their chosen specialty.

- If they face excessive competition in their niche, specialists can move up to become supernichers. For example, some cruise lines have made this transition, as have many boutique practices.

- Successful superniche players (that specialize by product and market)) are, in essence, monopolists in their niches, commanding 80-90% market share.

- Successful market growth (finding new markets for existing products) requires product strength, and successful product growth (developing new products for existing markets) requires market strength.

- Companies in the “ditch” exhibit the worst financial performance and have a very difficult time surviving.

- Ditch dwellers can emerge as big players by merging with one another, but only if there is no viable third ranked player to block them. General Motors achieved this in the early years of the automobile industry.

- A better strategy for ditch companies may be to seek a merger with a successful full line generalist. The ditch can be a very attractive source of bargains for full line generalists looking to rapidly boost market share.

- Ditch dwellers can emerge as specialists only if they are able to identify a defensible niche in which they have a sustainable competitive advantage through unique resource endowments. For example, Service Merchandize has reemerged as a jewelry specialist.

The evidence in support of these generalizations is strong and consistent. There is a powerful logic driving market evolution in this direction. The Rule of Three draws on fundamental truths about consumer psychology (e.g., the “evoked set” of brands typically considered by most consumers consists of three alternatives), competitive dynamics and the balance of power (see sidebar “Why Three?”).

Why Three?

Though our formulation of the “Rule of Three” is based primarily on empirical observation, there are a number of important reasons why a market structure based on three major players tends to be both viable and sustainable.

First, it is important to emphasize that this theory applies to markets rather than industries (as we normally define them). Thus, while aviation is an industry, commercial aviation is a distinct market within that industry. Markets are impacted by industrial dynamics (e.g., scale and scope economies) as well as consumer psychology. Market boundaries are thus defined by customer perceptions, wants and needs in addition to economic and technological concerns.

The primary logic in postulating the existence of three major players is that a market with three players is both more stable and more competitive than one with two players. With just two players, the outcome is either mutual destruction or collusion that is ultimately damaging to customers. Either scenario eventually leads to a de facto monopoly.

To create a balance or equilibrium, three entities are needed. With three main players, there is less predatory competition as well as a lower likelihood of collusion. In most markets, a coalition of two out of the three is strong enough to block any predatory intentions that the third might have. Just that threat prevents an attack, since the would-be “victim” can always seek the assistance of the third to counterbalance.

Why not more than three? Since only three players are needed to create a balance of power; the fourth player becomes expendable in the market’s push toward efficiency. More important, however, we believe that the Rule of Three is strongly linked with the theory of consumer “evoked sets,” the short-list of purchase options considered by a consumer. Research suggests that most consumers consider only three choices in making their purchases. Likewise, customers in industrial and commercial markets typically do not consider more than three suppliers. Getting into the “inner circle” for volume-oriented competitors is thus a matter of being one of the top three brands.

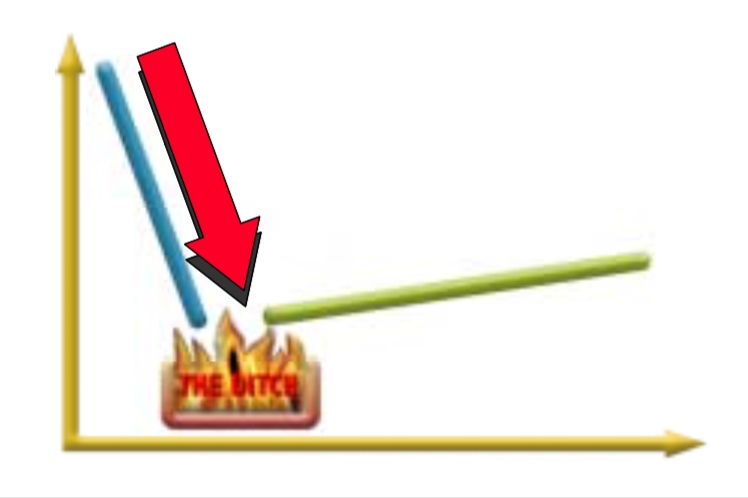

The Ditch

The Rule of Three posits a model of market competition in which two diametrically opposed strategies can be viable and successful. However, a veritable Bermuda Triangle of competitive strategy lies in the middle. Firms can generate attractive returns regardless of where they fall on the graph in Figure 1–except the ditch–provided they follow strategies appropriate to their position on the chart. Failing to do so has but one consequence: a slide into the ditch, and a long and possibly fatal attempt to climb back out. It is far easier to stay out of the ditch in the first place.

How Margin Players Get Pulled In

Margin-driven players are often lured into the ditch, tempted by the possibility of higher volumes. For example, in the global business of manufacturing writing instruments, Bic, a high volume French player driven by market share, dominates the mass market for ballpoint pens. The number two player in the mass market is PaperMate, followed by Scripto. On the other side of the graph are the margin- driven specialists: companies such as Mont Blanc, Waterman, Cross and many others, all of which operate with low volumes and high margins for their elegant offerings.

Margin-driven players are often lured into the ditch, tempted by the possibility of higher volumes. For example, in the global business of manufacturing writing instruments, Bic, a high volume French player driven by market share, dominates the mass market for ballpoint pens. The number two player in the mass market is PaperMate, followed by Scripto. On the other side of the graph are the margin- driven specialists: companies such as Mont Blanc, Waterman, Cross and many others, all of which operate with low volumes and high margins for their elegant offerings.

Consider what would happen if a fictional left-side pen manufacturer (Excalibur) were to become tempted to do business with a classic fictional right-side retailer (MegaMart). Here is how such a “marriage” of incompatibles might evolve:

Year 1 (The Selling of the Soul): Excalibur, under pressure from its shareholders to grow, seeks to broaden its market reach, and approaches MegaMart to carry its offerings. After much haggling, MegaMart agrees to carry the product, provided Excalibur lowers the price and invests in creating an electronic link with its ordering system. Excalibur, buoyed by the sudden growth in volume at a relatively modest reduction in its margins, reports record sales, market share, profits and stock price.

Year 2 (The Pound of Flesh): MegaMart asks Excalibur to further lower its price, hinting that it has alternative suppliers ready and waiting to offer comparable products on better terms. Excalibur, now hooked on the higher volumes, and having committed to an expansion of its manufacturing facilities, has little choice but to agree. Sales increase further, market share climbs, but profits head down. Investors, sensing distress, start selling.

Year 3 (Deja Vu All Over Again): Here we go again. Excalibur is once again asked by MegaMart to lower its price. The company pleads with the retailer that its has already taken as many costs as it can out of the system. Its high-quality metallic cylinder requires precision machining and expensive materials. Then comes the fateful question:

“Could you make it in plastic?”

The only way for Excalibur to salvage this situation is to decide which side of the graph it wants to play on. If it wants to go back to the left side, it must systematically exit certain markets and drop some products. It must reestablish its quality image. If, on the other hand, the firm wants to become a volume-drive player, it must recognize that its effort to climb the curve on the right-side will be immediately opposed by the No. 3 incumbent on that side: Scripto. A costly fight for market share will likely ensue, and profits will dry up completely for perhaps several years.

One fact is eminently clear: Excalibur cannot stay in the middle. The ditch is not a hospitable home for any competitor.

There are numerous examples of misguided attempts to grow out of specialty status. AMC, the automobile maker, went into the ditch after being a great niche player by trying to expand into a full-line of automobiles, though the Rule of Three was already in place in the industry. Lacking the resources to compete with the Big Three, AMC came up with a single car (the Hornet) masquerading as everything from an “econobox” to a luxury sedan. Not surprisingly, the strategy failed, and AMC was subsequently purchased by Chrysler.

How Volume Players Get Pushed In

On the right side of the graph, the most vulnerable is the No. 3 company, because it is closest to the ditch. In a growing market, the third full-line player continues to survive. However, when market growth slows, the two leaders aggressively fight for share. In the process, the No. 3 player (and any other aspiring full-line generalist) often gets pushed into the ditch. This is most common during tough economic times (such as the high inflation 1970s or the low-growth early 1990s), when overall market growth shrinks or is negative. This impels the No. 1 and No. 2 players to raise the competitive stakes and take market share away from the easiest target: the No. 3 player. For example:

On the right side of the graph, the most vulnerable is the No. 3 company, because it is closest to the ditch. In a growing market, the third full-line player continues to survive. However, when market growth slows, the two leaders aggressively fight for share. In the process, the No. 3 player (and any other aspiring full-line generalist) often gets pushed into the ditch. This is most common during tough economic times (such as the high inflation 1970s or the low-growth early 1990s), when overall market growth shrinks or is negative. This impels the No. 1 and No. 2 players to raise the competitive stakes and take market share away from the easiest target: the No. 3 player. For example:

Aircraft Manufacturing: In the recession of the late 1970s, the intense fight for market share between Boeing and McDonnell Douglas pushed Lockheed into the ditch. Lockheed, which had been #3 behind Boeing and McDonnell Douglas before the emergence of Airbus, was forced to exit the commercial aviation market, and focus on the military market. Trailing badly behind Boeing and Airbus in the globalized commercial aviation market in the mod 1990s, McDonnell Douglas sought a deal with Taiwan Aerospace to make the fast-growing Asian market its second “home” and particularly to position itself for the fast-growing China market (with its $20 billion in backlog orders). When the US government disallowed this deal, McDonnell Douglas’ options were limited; it could have emerged as a specialist producer of short-haul jets based on its MD-80 platform, or exited the commercial aviation market. In 1997, the company chose to accept a merger with Boeing, leaving the commercial aviation business without a third full line generalist. We believe this condition is temporary, and that a new full line generalist will eventually emerge.

Beer: In the late 1970s, Anheuser-Busch and Miller battled each other for market share; in the process No. 3 (Schlitz) and No. 4 (Pabst) were driven out. Now the combination of Coors and Strohs is positioning itself as the new No. 3 full-line player.

Autos: Chrysler’s descent into the ditch in the mid-1970s had little to do with Japanese competition and everything to do with the fight between GM and Ford. After the 1974-75 energy crisis, GM redesigned the Chevrolet Caprice, a car that had great fuel efficiency and was rated by Consumer Reports as a “Best Buy” for several years running. As a result, GM’s market share in full-size cars jumped significantly. Ford was able to keep pace, but Chrysler couldn’t. It went into the ditch, and then reemerged following its bailout as a marginal full-line player with an emphasis on minivans. Chrysler could have remained in the ditch, giving Toyota or Honda an opportunity to become the No. 3 player in the U.S. market. However, Chrysler pulled ahead through its acquisition of AMC from Renault, while Honda failed to rapidly expand its product line to include minivans and sports utility vehicles.

In the short run, the third player may exit during market slowdowns or period of intense rivalry. At the end of such a period, there is usually another third player who emerges–usually not the one that left.

Importantly, niche players are not significantly affected by the competitive tumult among the generalists. The competitive challenge from full-line generalists primarily affects other generalists and would-be generalists. Successful specialists are generally secure in their own niches. For example, the beer battles left microbreweries unscathed, the cola wars had little impact on sports drink maker Gatorade, and corporate jet makers prospered even as the generalists fought for dominance in the commercial aviation market.

The Rule of Three and Globalization

Artificial market structures outside Europe and North America are also giving way to the “natural” market structure represented by the Rule of Three. For example, the great trading houses of Japan (such as Mitsubishi, Mitsui and Sumitomo) have long participated in numerous business sectors, supporting weaker businesses through interlocking shareholdings (the “keiretsu” system, which creates a closed market within the overall free market). This has shielded many poor performing companies from market forces, and as a result has kept too many weak companies afloat in the market. In recent times, however, this system has finally started to break down. The discipline of a truly market-driven economy is forcing weak companies to exit or get acquired, often by global competitors.

In South Korea, the huge diversified “chaebol” such as Hyundai, Daewoo, Samsung and LG (Lucky- Goldstar) have traditionally used their enormous clout with the government to maintain their leadership in virtually every major economic sector. The Asian economic crisis of 1997 and the conditions of the subsequent IMF bailout of South Korea started the process of breaking down this cozy relationship, and bringing market forces to bear to a greater extent.

In India, most major industries have been dominated by the large industrial houses, many of them family controlled. Until a few years ago, foreign companies faced stringent restrictions on their ability to participate in the Indian economy. Capacity rationalization was nearly impossible to achieve as a result of licensing and the inability to “downsize” (reduce the labor force) when market conditions so dictated. All of this is now changing, as economic liberalization and the demise of isolationist economic thinking have triggered a shift toward more freely competitive markets.

The important and ongoing shift toward global markets leads to a significant corollary of the Rule of Three: No matter how large the market, the Rule of Three prevails. In other words, when the scope of a market expands–whether from local to regional, regional to national, or national to global–the Rule of Three prevails, and further consolidation and industry restructuring become inevitable. Many nationally or regionally dominant companies find themselves trailing badly once the market globalizes.

For example, though U.S. banks are still prohibited from true, no-holds-barred interstate banking, they are working around those restrictions with holding company structures making de facto regional banking increasingly the norm. Consolidation through mergers and acquisitions is proceeding apace towards a Rule of Three market structure. Such a structure already exists in Germany and Switzerland. Likewise, the U.S. airline market has moved from a regional to national scope, and the process of sorting out full-line players from geographic specialists is underway, with the likely survivors being American, United and Delta. Cable television franchises, once the most local type of business, are consolidating into large regional players, with national and international consolidation following close behind.

Because local or regional markets are relatively rare (and are usually maintained only through regulatory mandate), the most important transition is when a market organized on a country-by-country basis moves towards becoming truly global. A distinct pattern emerges when markets move to this level, offering some of the most powerful evidence for the Rule of Three.

When the market globalizes, many full-line generalists that were previously viable as such in their secure home markets are unable to repeat that success in a global context. When this happens, we usually find that there are three survivors globallytypically, but not necessarily, one from each of the three major economic zones of the world: North America, Western Europe and the Asia-Pacific region. To survive as a global full-line generalist, a company has to be strong in at least two of the three legs of this triad.

If a country has a large stake in an industry, it may be home to two or even all three full-line players. This was true in the aerospace market in the U.S., where the Defense Department essentially bankrolled the industry’s technological superiority. Japan targeted industries such as consumer electronics, steel, shipbuilding and several others. In the long run, however, political considerations make it unlikely that one country could dominate a significant market globally. Thus, in the aerospace market, the historical dominance by U.S. companies led several European governments to boost Airbus to a position of global prominence.

With globalization, the No. 1 company in each of the three triad markets is best positioned to survive as a global full-line generalist. Other players either go through mergers as a consequence of global consolidation, or they selectively exit certain businesses to become product or market specialist, often by geographic region.

In consumer electronics, the U.S. market is now experiencing a fierce fight for market share between the Japanese (Matsushita/Panasonic and Sony) and the Europeans (Philips/Magnavox and Thomson/RCA/GE). This battle will determine which players survive as global full-line generalists. The U.S. presents an ideal battleground because there is no company with a “home court advantage;” since there is no major domestic consumer electronics player, there is little danger of government intervention.

In the airline market, globalization is proceeding simultaneously with the market’s evolution towards national competition after deregulation. Given the numerous restrictions on foreign ownership of airlines, and in the absence of true “open skies” competition, the global industry is organizing into three big alliances: Star Alliance (Air Canada, Lufthansa German Airlines, SAS, United Airlines and several others), Oneworld (Aer Lingus, American Airlines, British Airways, Cathay Pacific, Finnair, Iberia, LanChile and Qantas) and Skyteam (Delta, Air France, Aeromexico, Alitalia, CSA Czech Airlines and Korean Air Lines).

Strategies for Generalists vs Specialists

Full-line generalists are first and foremost volume-driven players, while specialists tend to be margin-driven. In addition, successful generalists and specialists follow different strategies and have very different operating characteristics, as depicted in Table 1.

| Characteristics | Generalists | Specialists |

| Sources of Advantage | • Size x Speed | • Selectivity x Service |

| Cost Structure | • High Fixed Costs | • High Variable Costs |

| Scope of Offerings | • Full Line of Products | • Limited Line of Products |

| Positioning and Branding | • One Stop Shop Positioning with Single Brand (Corporate) or Dual (Upscale and Mainstream) Brand Identity | • Target Market Positioning, Multiple Brand Identity |

| Distribution Channels | • Multiple Channels | • Focused Channels |

| Organization and Operations | • Integrated Organization, Shared Operations

• Networks and Alliances |

• Multibusiness Organization, Dedicated Operations

• Vertical Integration |

Table 1: Generalists versus Specialists

Sources of Advantage

Because they are large, volume-driven players, generalists depend on economies of scale and the potential for selective cross-subsidization for much of their competitive advantage. They have large fixed assets in place, and their success depends heavily on their ability to maximize use of those assets. Such players create (and constantly must improve) an “asset-turns” advantage–the ability to reuse the same large variable and especially fixed assets (which could be retail floor space, a large factory, a national telecommunications network or financial assets such as working capital and inventory) continuously and efficiently.

Generalists achieve their value positioning through internal synergies, such as integrated operations, and external synergies, such as a single corporate identity. The cost savings enabled by these two factors, along with efficiency advantages derived from scale economies, enable generalists to offer superior value to many customer groups.

Specialists, in contrast, tend to emphasize service and selectivity rather than size and speed. Most specialists are also margin-driven players, due to the fact that they tend not to invest heavily in fixed costs.1 Since variable costs are high, and sales volumes are low, profitability is driven by increasing the margin, either by raising the price (accompanied by further differentiation of the product), or lowering costs through greater efficiency.

Never the Twain Shall Meet

Full-line generalists and product/market specialists have inherently different approaches to business that rarely mix well. Specialist manufacturers who start selling through generalist retailers are headed for trouble (see sidebar on Excalibur and MegaMart earlier). Likewise, it is almost impossible for generalists and specialists to work together in an alliance. The inherent contradictions between a margin-driven and a volume-driven player are too great to be readily overcome.

Generalists who try to run specialty businesses in addition to their core business find that they have no talent for it. Kmart’s attempt to foster a range of specialty businesses, such as Walden Books and Sports Authority, failed.

The only way generalists can succeed with such a strategy is by maintaining strict separation between the two sides. Any attempts at extracting synergy between the operations (by creating overlapping assortments, sharing brand names etc.) will failthey dilute the uniqueness and specialty nature of the specialist. Woolworth has been only moderately successful running a wide variety of specialty retail chains.

Of course, the absence of synergies begs the question of why a stable of successful businesses should be saddled with added corporate overhead and sluggish bureaucracyquestions answered mostly in the

negative during the 1980s, when numerous diversified companies were acquired in hostile takeovers and then split up.

Cost Structure

The cost structure of a full-line player is dominated by fixed costs: extensive manufacturing facilities, sophisticated flexible manufacturing systems, huge amounts of retail floor space, hundreds of airplanes or hotels, etc. For the incremental transaction, variable costs tend to be low. The opposite is true for most successful specialists: they invest in a minimum of fixed assets, and are thus able to scale their costs down rapidly if needed.

Scope of Offerings

Successful generalists offer a wide range of products and services, and are able to meet the needs of customers for ancillary products as well, either through horizontal integration or alliances with other firms. Specialists, on the other hand, either offer a wide range of products to a well-defined market segment (market specialists) or a narrow range of products to all comers (product specialists, such as the various “category killers” in retailingStaples, Toys ‘R Us, Tower Records).

Positioning and Branding

Generalists must pursue a broad market positioning and promote a single corporate identity. Broad-based Japanese companies have shown us for decades that brand names are far more powerful when defined broadly and applied widely (such as Yamaha, Panasonic and Mitsubishi). Full-line generalists must use umbrella branding, offering varied products to diverse segments under a common market identity. The corporate positioning must be broad enough to allow for wide applicability across products and segments.

The Innovation Leader: No. 3

For years, RC Cola was the most innovative of the big three soft drink companies. It was the first to use aluminum cans (a move that took Coke years to respond to) and the first to introduce a diet cola (Diet- Rite), playing on Coke’s historical reluctance to change its formula.

In the automobile industry, perennial #3 Chrysler was known for decades as an innovative engineering company, and then as a leader in innovative product design. It invented the minivan, and sold over four million of them in a decade. It reintroduced the convertible to the mass market, and then pioneered the successful “cab forward” design.

In the long-distance telephone market, the No. 3 player is Sprint. The company has a history of pioneering innovations, most of them related to its technology. It was the first company to invest heavily in fiber optics, creating the first fully digital phone network. Sprint was the first telecommunications company to combine long distance, local and cellular services, a move since mimicked by its rivals. It was the first to introduce ATM technology into its network, and the first to offer voice-activated calling. Sprint’s relative lack of market success has been due to the extraordinary marketing prowess of its chief rival MCI.

Since they cannot afford to play by the rules of Nos. 1 and 2, No. 3 companies must compete on new flanks. For example, RC Cola looked for something Coke could not easily duplicate. They decided to attack Coke in an area where it had little flexibility: its bottling operations. Coke utilized thick, recyclable glass bottles. RC Cola introduced the aluminum can. It required a huge investment for Coke to make the change to aluminum; they couldn’t do it immediately.

A second move by RC Cola was predicated on its belief that Coke would never change its recipe. RC Cola invented Diet-Rite, the first low-calorie soft drink. Pepsi countered very quickly and Coke responded much later with Tab, which was not a big success.

Specialists must be positioned differently than generalists. Product specialists need an identity that is virtually synonymous with a product category (or sub-category), whereas market specialists have to define themselves almost entirely in terms of their (ideal) customers. Since each brand stands for something distinct, specialists with more than one focus must keep the identity of each separate.

Distribution Channels

To attain maximum market coverage, generalists must be easily accessible to all customers. They thus utilize complex hybrid distribution systems, while specialty businesses tend to use much more focused distribution channels. Importantly, specialty businesses typically distribute their products through specialty retailers, rather than through volume-driven mass merchandisers.

Organization and Operations

Successful volume players today also focus on integrating as many aspects of their organization as possible, striving for seamlessness and shared operations. This avoids duplication of effort and leads to higher asset turns. Such companies also make extensive use of “flexible” fixed assets, i.e. those that can be readily reconfigured to meet different kinds of demand.

Specialty businesses tend to be divisionalized rather than integrated organizations, since synergies across businesses are minimal. Each business within the umbrella has its own dedicated operations.

When the Rule of Three Does Not Apply

The Rule of Three applies wherever competitive market forces are allowed to determine market structure with only minor regulatory and technological impediments. It would, therefore, not apply in markets where the following factors are significant:

- Regulation. If regulatory policies hinder market consolidation (as they have in Japan) or allow for the existence of “natural” monopolies (as was the case with the local telecommunications market in the U.S.), the Rule of Three is not operational. With deregulation, it comes into play, as with the U.S. airline, trucking and telecommunications industries.

- Exclusive rights. If patents and trademarks are major factors in a market, it must be viewed as a collection of sub-monopolies, and is thus not subject to market forces. In the chemical and pharmaceuticals markets, therefore, we are less likely to see the Rule of Three govern market evolution. However, in recent years, the pharmaceutical industry has seen a large number of mergers and appears to be gradually moving toward the Rule of Three; this is due to the fact that large pharmaceutical firms are now participating in the growing generic sector as well as patented drugs, and patent-based sub-monopolies are being eroded as firms target the same therapeutic class with multiple drug formulations.

- Licensed economy: The Rule of Three cannot operate in economies in which companies are not free to adjust their production levels up or down based on market conditions. With the passing of India’s infamous “license Raj” of old, market forces have come increasingly to the fore, leading many companies to achieve greater economies of scale through production growth as well as mergers. The WTO has been a prime driver in raising the competitive intensity of industries internally as well as from the outside.

- Major barriers to trade and foreign ownership of assets. In this case, we are likely to see the Rule of Three operate at the national level but not at the global level. The Rule of Three may still be seen in the formation of global groups or alliances, as we believe is likely to occur in the global telecommunications market.

- Markets with a high degree of vertical integration. To the extent that certain customer groups are captive to in-house suppliers or vice-versa, the emergence of three full-line players in the supplier market is unlikely. Vertical integration does not allow competitive market forces to operate. It ties up suppliers and customers internally so they are not free to buy or sell in the open market.

- Markets with combined ownership and management. If ownership and management are combined, as in the case of professional services, the market process is not allowed to work. Ownership creates an emotional attachment, and inhibits rational economic decision-making.

When these barriers begin to fall, markets start moving towards the Rule of Three.

Conclusion

The Rule of Three is much more than an interesting theoretical construct; it is a powerful empirical reality that must be factored into corporate strategizing. Understanding the likely end-points of market evolution is critical to the ability of executives to develop strategies that will result in success.

The lure of greater market share to niche players is a powerful one, and has caused many successful specialist companies to sacrifice their distinguishing characteristics and dilute their competencies in a headlong pursuit of growth, only to end up in the “ditch.” As we have pointed out, such strategies are only viable if a clear (i.e. unblocked) opportunity to occupy a generalist position exists. If not, firms are generally far better off deploying the same resources into a geographic expansion within existing niches, or creating new niches.

Just as many specialist companies wrongly aspire to be generalists, many struggling generalists would deliver greater value to their stakeholders by merging with other generalists or reverting to specialist status. Profitable share matters much more than market share per se; as a senior Chrysler executive put it, “We would rather sell two cars at a profit than three at a loss.” Eminently reasonable and seemingly incontestable though that concept may be, too many companies fail to grasp it.

Ultimately, the Rule of Three is about the search for the highest level of operating efficiency in a competitive market. Industries with four or more major players, as well as those with two or fewer, tend to be less efficient than those with three major players. The role of the government is to ensure that free market conditions do indeed prevail, to allow industry rationalization and consolidation to occur naturally, and to step in when an industry seeks to consolidate too far, i.e., to a level where fewer than three players control the lion’s share.

The greatest impact and potential dislocations arising from the Rule of Three occur when an industry makes a major geographic transition–from regional to national, or even more dramatically, from national to global.

The impact of this transition on a number of industries, including tires, appliances, automobiles, telecommunications and hotels has been the emergence of a new core of inner circle companies, with, at times, surprising winners and losers.

Finally, an implicit understanding of the Rule of Three lies behind General Electric’s well-known “Number 1 or Number 2” approach to restructuring in the 1980s. When Jack Welch laid down these guidelines–that GE would have to be No. 1 or No. 2 in any business that it remained in–he was recognizing the constant pressures and pulls on businesses that are No. 3 in their market. The strategic implications of the Rule of Three are many and varied, however, and thus go considerably beyond this dictum.

As more markets become globalized or get transformed through technology in coming years, managers everywhere will have to reassess their corporate positioning and strategic goals. For some, this will spell a once-in-a-lifetime opportunity to seize the initiative and firmly establish their companies on a larger stage. For many others, it will require hard thinking about strategic choices, and the courage to make painful but necessary decisions about markets not served and products not offered.

- Even in service industries where fixed costs tend to dominate, such as the airlines industry, a specialist player might choose to lease the physical asset, or arrange for the costs of the asset to be linked to usage levels. ↩

2 Comments